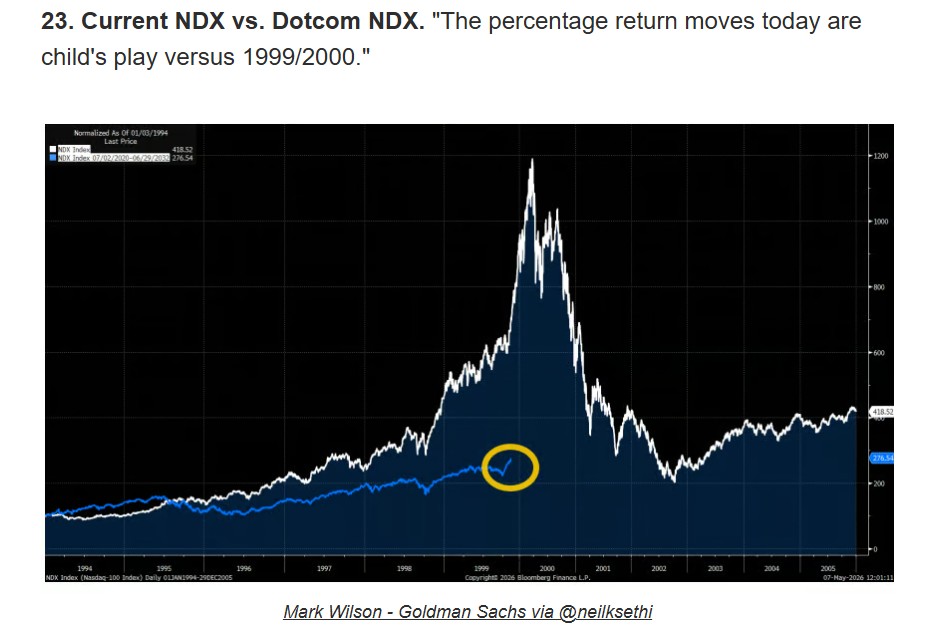

In 2008 I set out a roadmap for the next 25 years. I’ve repeatedly written about this and so far, the roadmap has proven to be correct all along the way. This secular bull market that began in 2011 is now morphing into an AI & robotics & innovative technology bubble that already mimics the prior Dot.com technology bubble of the 1990’s. In that Dot.com bubble, e-commerce stocks gained 400% in just the final few months.

Bubbles are to be bought with both hands; they are NOT to be feared. All bubbles have naysayers and they all experience actual but temporary pullbacks (like now). The only important thing is that one just has to be able to recognize the actual secular top when it is forming (this has been a 40-year study for me). In my opinion, we are currently nowhere near the secular bull market top… with the current downward price action merely being a temporary and routine pullback.

I believe that we are now, in 2026, repeating the year of 1998 which is when the Asian Financial Crisis took hold of the global economy, especially hitting the technology sector. In that year, Asian markets dropped 75%.

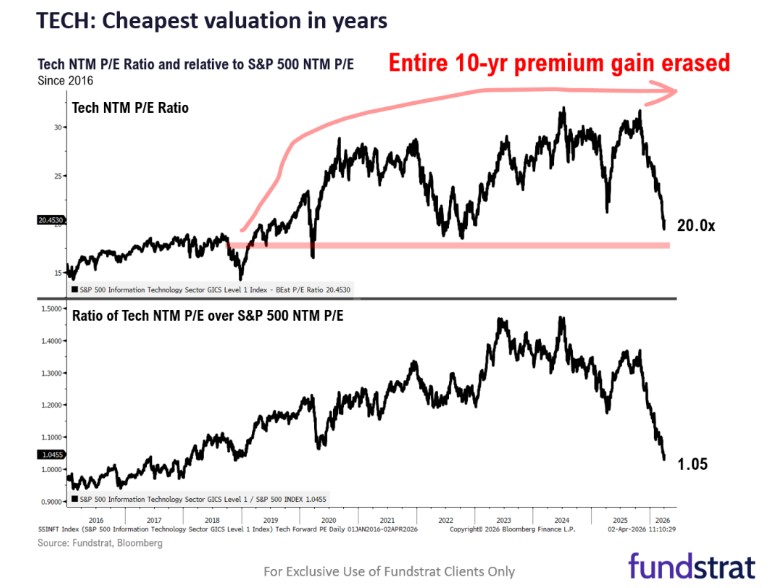

Today, in 2026, Asian markets are down (IE, Korea) by roughly 40% in July and the big hit is, once again, in the technology sector. U.S. technology stocks are also temporarily down, but half the amount (while some other sectors are doing well, and that is why diversification is important). We are very close to the bottom of this temporary pullback that will soon be behind us.

In 1998 the market pulled back and bottomed in an uncommon “V” pattern (that we have seen so often in the past few years). Bottoms are normally volatile things that bottom in a prolonged “W” pattern where the bottom does not form quickly and it “retests” itself. When the current weakness is over, within two months(?), and if we hit yet another “V” shaped bottom, which I’m betting on, then investors will finally believe that ALL bottoms are very temporary and that they all recover quickly and that they are all events to just patiently sit through… after all, pullbacks are paper losses only unless one sells at the bottom of the pullback. This “never sell” belief will begin to permeate the investment world and it will lead to most investors refusing to sell during high-risk periods and it will first lead to the multi-year parabolic bubble formation (because there will be many more buyers than sellers of stocks)… and then we get the subsequent (big & prolonged) stock market crash that will manifest as this current bubble finally deflates. This future crash, stilll years away, MUST be avoided.

So, I’m looking at another couple of difficult months, aided and abetted by the Trump tariff inflation and by President Trump’s (impossible to actually win) war against Iran causing even more continued inflation, and by the weakness that always occurs during a President’s second year in office, and by the likely chaos around the 2026 election, and by the often-weak summer months of June-September… when investors are off vacationing. A bundle of weakness causing several months of weakness in the stock market, especially in technology since it has been leading the market higher.

Stock market down today:

.

But what’s coming? The final two years of the Dot.com bubble (1999 & 2000) were incredibly strong for investors and, in my opinion, the coming two years will be a redux of that super-bullish period, only stronger.

So, buckle up!

.

.

Thanks for reading!

MarketCycle Wealth Management has, for four decades now, continually studied how to exploit bubbles and their subsequent crashes. Allow us to navigate your investment account through what may prove to be an exceptionally profitable period. There is a contact tab on our website.

.