.

The stock market is showing incredible internal strength. It was weak and has now strengthened. Usually when the stock market has been weak but then improves, the economy itself (and home prices and the consumer) then becomes temporarily weaker as stocks rise up off of their bottom. That is happening now: stronger stocks, weaker economy; the two do not move in tandem.

And then there is Trump.

President Trump naturally spent the weekend threatening high tariffs again and he (temporarily) followed through on Monday with attacks on some of our closest allies (and the Dow stock index is down over 600 points as I type this today). Frankly, I just wish that he would concentrate on his golf game; he certainly doesn’t understand how tariffs or the economy work. Volatility, with drawdowns, is the result in the near-term… but it won’t last; the stronger stock market will eventually win.

Trump’s “Big Beautiful Bill” just passed and is now signed into law… and please don’t shoot the messenger: The rich get lower taxes and more loopholes; the poor get higher taxes and higher food & health care costs and more hurdles to jump. Hungry poor children lose their school lunch assistance. Hospitals and clean energy suffer under the new bill. Trump gets endless money to build prison camps for legal naturalized citizens and illegal migrant workers, not just in the Everglades of Florida, but his stated plan is to build them all across the country. Social Security itself was weakened by the bill since the tax cut for some seniors comes directly out of the Social Security system’s coffers… but if you work after qualifying for Social Security, and if you earn too much, you are penalized. Of course, the deficit quickly goes up by another $3.3-Trillion; the United States is now $37-Trillion in DEBT.

-$37,000,000,000,000

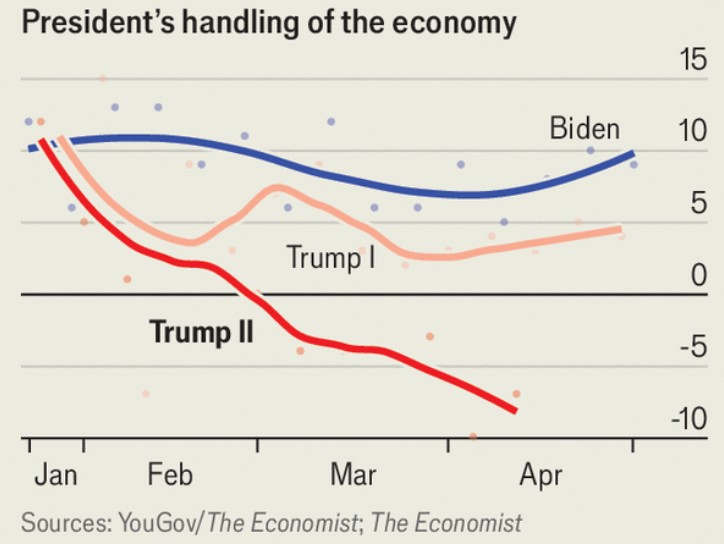

We may get some near term (tariff caused) economic weakness & turbulence plus continued weakness in home prices and consumer spending… with weakness ending in the late Fall of this year? Below is a weekend quote from President Trump. I don’t know about you, but I can’t figure it out. I do know that when push comes to shove (if the stock market suddenly drops), Trump will cave in on tariffs, continuing the TACO trade. Please remember that tariffs are NOT paid by the foreign country… they are ultimately paid by YOU in the form of higher prices. And we have to remember that tariffs haven’t really happened yet… July 9th is the deadline… or is it August 1st? (Quote courtesy of Fortune via Yahoo News):

.

Tariffs impact stock sectors differently, with the below sectors on the left being the safest in a “tariff world.” REITs and financials (banks) and gold & crypto would also be on the left. MarketCycle’s client accounts are strongly leaning toward the (green) left on this chart (Chart courtesy of Apollo Global):

____________________

Everything that is needed for the stock market to run higher is now in place since corporations no longer need to worry about regulations or any damage to our environment. And the super-bull market will now broaden out and pick up speed and, in my opinion, it will eventually go parabolic for longer than people would currently believe possible.

We are in the final few years, the strongest years, of a 20-year secular stock bull that started 16.5 years ago. The current period will mimic 1997 to 2000, where Internet stocks went sky high and generated outstanding profits.

And the bear market that always follows at the end of all 20-year secular bull periods is a real killer. The last example was the Dot.com Crash in 2000 which was followed by 10 years of weakness (and the crash was copied again in the Financial Crash of 2008). If I am right, the coming crash at the end of this decade may totally reset both politics and the economy (and maybe the U.S. even just defaults on its debt or we allow the Federal Reserve to “buy” all of our debt and permanently hide it in their non-audited books?)… a chance to start over, including a new gold backed digital currency since the U.S. owns most of the world’s physical gold; a chance to do things differently and better. Crisis leads to opportunity.

During the next few years, it will be innovative technology and particularly AI & robotics and crypto & blockchain (and inflation assets) that will lead the way to great profits. By 2028 the stock market may be moving parabolically higher and this might even cause people to (dangerously) take out second mortgages on their homes and to borrow money from brokerage houses in order to toss the money at the stock market.

There will be some bumps along the road, perhaps a temporary larger pullback in 2027, but investors just need to hang on until the very end. My job is to spot the end times and then to switch gears AT THE RIGHT TIME in order to profit from the destined big bear market that will then be due.

Technology is fairly immune to tariffs and interest rates and inflation. Technology has been leading the market higher, BUT it is still in the early stages of its ascent. Innovative technology, just now at the middle of its “S” curve cycle, is likely to be a particularly strong asset during the coming few years. AI and robotics technology are both extremely important, as are the smaller utilities that run AI data centers and the big banks and private credit companies that fund the new technology startups. Effective July 1st of this year, the market is suddenly broadening out while the USDollar is less strong, which means that we now have an opportunity to successfully buy innovative & disruptive technology in all cap-sizes and from all countries, including Japan and Asia.

Interestingly and hard to believe (and fact checked) Amazon literally just created its millionth robot (imagine, Amazon now has 1,000,000 factory robots!). Meta has just hired a giant “who’s who” list of AI builders. It’s happening, so one might want to buy into the stock market and just hold on! (Chart courtesy of TechCrunch)

.

I personally believe that the need to create an intelligence is built into our DNA and, as a sort of “manifest destiny,” it cannot be stopped. So, going forward the BIG story will be artificial intelligence (and robotics). The rush into AI will likely push the stock market to unbelievable heights over the next few years. AI & robotics will be a key factor during the remainder of our lives (and beyond), no matter how the stock market reacts to the AI & robotics trade in later years. I now use AI every day of my life.

This important chart below shows the potential of what may be THE great technology super-bull that is still in its early stages. My bet is that the “AI trade” goes parabolic for a profitable and prolonged period. Going forward, every time that someone on Wall Street declares that we are in an AI technology bubble and that we should “watch out,” just laugh and ignore them… they have no clue as to how big a bubble can become. In my opinion, this AI bull will be big.

The current wave may prove to be the big one… we’d currently be just about where the question mark is. (Chart courtesy of Benedict Evans, a technology expert based out of London):

.

In general, MarketCycle’s client accounts hold the following positions (there may be some accounts that are too small to hold all positions and custodial trusts for minors and corporate accounts cannot hold any “esoteric” positions):

- Gold bullion

- Private credit funding for technology companies (half floating-rate & half fixed-rate, 100% secured, paying 7% interest)

- Bitcoin & MicroStrategy (our bitcoin ETF pays 28% interest without cutting into profit gains and MicroStrategy is cornering the market in Bitcoin)

- Managed futures (long-short global interest rates, global currencies and commodities, but does not hold stocks… a great diversifier and a big help during inflationary periods)

- Developed market growth stocks (growth = strong)

- Small-cap momentum (momentum = trending strong)

- Mid-cap momentum (cap = size of the corporation)

- Large-cap momentum

- U.S. Technology sector

- Global innovative technology

- Global artificial intelligence

- Global robotics

- U.S. large-cap banks (they fund new IPOs and mergers)

- U.S. small-cap to mid-cap utilities (they supply energy to AI data centers)

.

That’s it, thanks for reading!

.

.

MarketCycle Wealth Management, for a low fee, manages brokerage accounts for the general public… in the United States and globally. There is a contact tab at the top of our main website. We strive to earn our keep.

Our REPORT site can be reached via the connecting link on our website.

.

.